Car Insurance: Protecting Your Ride and Your Peace of Mind

Learn everything there is to know about auto insurance, from the fundamentals to the nitty-gritty details. Learn how to select the ideal coverage and save money on your premiums by following these instructions. Learn the reasons why purchasing auto insurance is necessary to protect yourself and your vehicle.

Introduction

Insurance for your vehicle is not only required by law in most jurisdictions; it is also an essential instrument for protecting your financial well-being and ensuring that you are protected in the event of an accident or unforeseen damages. It doesn't matter if you've been behind the wheel for years or just bought your first automobile; having a solid understanding of auto insurance is essential for making educated decisions regarding your coverage. This comprehensive guide strives to provide expert views, helpful recommendations, and in-depth information on car insurance, with the goal of assisting you in navigating the complex world of auto insurance with ease.

Car Insurance: What Is It and Why Do You Need It?

You, as the policyholder, enter into a legally binding contract with an insurance company when you get auto insurance. As part of this arrangement, you pay a premium in exchange for protection against a range of hazards. This protection may involve safeguarding against mishaps, theft, and vandalism, in addition to liability protection in the event that another person sustains bodily injury or property damage. Having auto insurance is not only a required in many different countries, but it also provides piece of mind by guaranteeing that you won't face financial devastation as a result of unforeseen incidents on the road. This is because auto insurance protects you from lawsuits, medical expenses, and property damage.

Types of Car Insurance Policies

Although it can be confusing to learn about all of the many kinds of auto insurance policies, it is really necessary to locate the coverage that best meets your requirements. The following is a list of the primary categories of auto insurance policies:

- Liability Insurance: If you are found to be at fault in an accident, this kind of insurance will pay for the harm that you have caused to other people. In most cases, it covers legal responsibility for both injuries to people and damage to property.

- Collision Insurance: If you are in an accident, regardless of responsibility, the cost of repairs or replacement for your car will be covered by collision insurance.

- Comprehensive Insurance: Non-collision incidents, such as theft, vandalism, fire, or natural calamities, are covered by comprehensive insurance.

- Uninsured/Underinsured Motorist Coverage: If you are in an accident with a motorist who does not have sufficient insurance or none at all, this policy will protect you.

- Personal Injury Protection (PIP): PIP pays for your medical care and those of your passengers no matter who was at fault in the collision.

- Gap Insurance: If your automobile is written off, but you still owe money on your loan or lease, gap insurance will cover the difference.

- Usage-Based Insurance: The premiums for this coverage—also called "telematics insurance"—are determined in part by how safely and responsibly you drive.

You may also like : "Life Insurance: Protecting Your Future and Loved Ones"

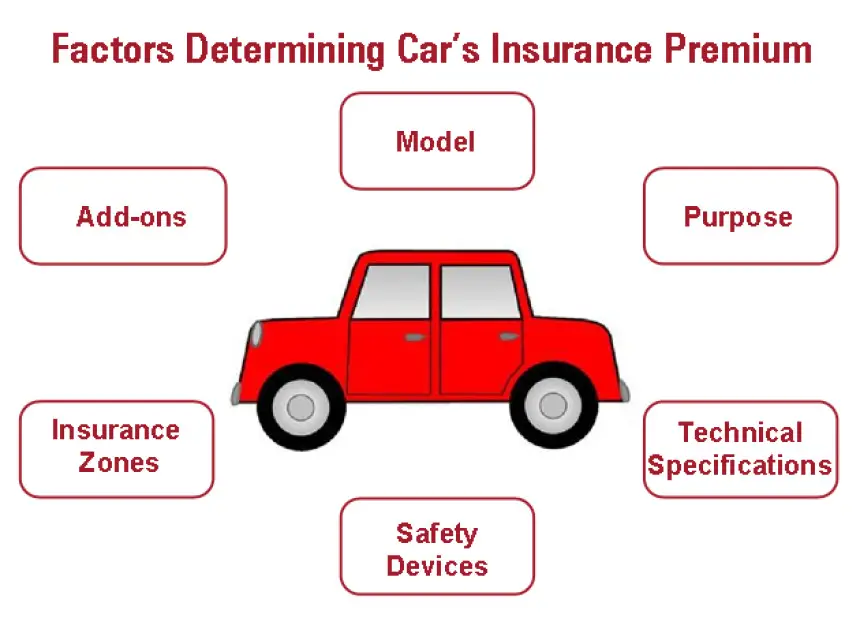

Factors Affecting Car Insurance Premiums

The cost of auto insurance premiums varies widely from one person to the next depending on a number of criteria. If you take the time to learn about the following, you may be able to lower your insurance premiums:

- Driving Record: Insurance rates tend to be more affordable for drivers with spotless records, free of accidents and moving infractions.

- Age and Gender: Insurance rates tend to be higher for young, inexperienced drivers. As a result of statistical risk variables, men drivers also tend to pay more.

- Location: Insurance premiums may be more expensive in urban centers or other places with a higher incidence of accidents.

- Car Make and Model: A person's premium can vary depending on the vehicle they drive. Insurance premiums may be higher for sports cars and luxury automobiles.

- Annual Mileage: The bigger the risk associated with an individual driver, the higher their insurance premiums may be.

- Credit Score: Insurance firms may use credit scores as a factor in determining rates in some areas.

- Deductible Amount: Choosing a higher deductible will reduce monthly premium payments, but it will increase your out-of-pocket costs in the case of an insurance payout.

Tips for Finding the Right Car Insurance Policy

It might be difficult to shop for auto insurance, but these pointers can help you narrow down your options and select the policy that's suitable for you:

- Assess Your Needs: When choosing a policy, it's important to think about how often you drive, how much your car is worth, and how much money you have.

- Compare Quotes: Compare insurance premiums by requesting quotations from several different companies.

- Bundle Policies: Bundling your auto and house or apartment insurance policies might save you money, as many providers provide discounts for doing so.

- Check for Discounts: Find out if there are any safe-driving, loyalty, or car-safety-feature-related discounts you may take advantage of.

- Read the Fine Print: Learn the ins and outs of the insurance, such as the coverage levels, any potential gaps, and the steps necessary to file a claim.

- Review Customer Reviews: You can learn a lot about a company's responsiveness to claims by reading reviews written by satisfied consumers.

- Seek Expert Advice: Talk to your insurance agent or broker for clarification on any details you don't understand.

The Cost-Benefit Analysis of Car Insurance

Consider the costs and benefits before making a decision about auto insurance. Although auto insurance rates may seem like an unnecessary outlay of funds, the advantages of having car insurance far outweigh the costs:

- Financial Protection: Car insurance provides a safety net against significant financial losses resulting from accidents or damages.

- Legal Compliance: Most regions mandate minimum car insurance requirements, and being insured ensures you comply with the law.

- Peace of Mind: Knowing you're protected on the road brings peace of mind, reducing stress and anxiety while driving.

- Asset Protection: If you have a car loan or lease, insurance protects the asset and ensures you won't be burdened with debt in case of a total loss.

- Medical Coverage: Personal Injury Protection (PIP) can cover medical expenses, saving you from substantial medical bills.

- Third-Party Liability: Liability insurance protects you from costly lawsuits if you cause bodily injury or property damage to others.

- Coverage for Unforeseen Events: Comprehensive insurance safeguards your car against theft, natural disasters, and other non-collision incidents.

You may also like : "Health Insurance: A Comprehensive Guide to Securing Your Well-being"

Understanding No-Fault Insurance

When an accident occurs, no matter who was at fault, the insurance company for each motorist pays for its policyholder's medical bills and property damage. The time it takes to settle legal claims is one of the primary goals of this system. No-fault insurance rules, however, might vary widely from one state to the next. Some key points to understand about no-fault insurance include:

- The idea of "no-fault" does not guarantee that you will not be held legally responsible for an accident.

- While no-fault insurance may be mandatory in some areas, in others it may be an extra cost.

- Medical bills, lost earnings, and other costs associated with an accident are often covered by no-fault insurance.

Choosing the Right Deductible Amount

Your insurance won't kick in until you've met your deductible, the amount you're responsible for paying out of pocket. It is essential to strike a balance between premium costs and potential out-of-pocket expenses by choosing an appropriate deductible amount:

- Low Deductible: Opting for a low deductible means you'll have lower upfront costs in case of a claim, but your premiums will likely be higher.

- High Deductible: Choosing a high deductible results in lower premiums but requires you to pay more out-of-pocket if you need to make a claim.

Before settling on a deductible, it's important to take stock of your financial circumstances and your comfort level with risk.

Navigating the Claims Process

Filing an insurance claim can be stressful, but knowing the steps involved can make the process smoother:

- Report the Incident: Contact your insurance provider immediately after an accident or incident to report the details.

- Provide Information: Be prepared to provide all relevant information, including details of the incident and any involved parties.

- Document the Scene: If possible, take photos of the accident scene and gather contact information from witnesses.

- Cooperate with Insurer: Work closely with your insurance adjuster, providing any necessary documentation or evidence.

- Repair Estimates: Obtain repair estimates from authorized repair shops for approval by your insurer.

- Claims Settlement: Once the claims process is complete, you will receive compensation based on your coverage and the determined fault.

Conclusion

Protecting yourself and your vehicle on the road is a top priority, making auto insurance more than simply a need. You may better manage your coverage needs and costs by learning about the various auto insurance policies available to you, the factors that affect your premiums, and the steps involved in filing a claim. Finding the right auto insurance policy requires careful consideration of your needs, research, and the assistance of professionals. Being prepared and well-informed will allow you to travel with the confidence that comes from knowing you and your belongings are safe.

You may also like : "How to Reduce Your Car Insurance Premiums"

Frequently Asked Questions (FAQs)

Q1} What Factors Affect Car Insurance Premiums?

- Car insurance premiums are influenced by various factors, including your driving record, age, location, car make and model, annual mileage, credit score, and deductible amount.

Q2} Is Car Insurance Mandatory?

- In most regions, car insurance is mandatory to legally operate a vehicle on public roads. Failure to have valid insurance can result in fines, license suspension, or vehicle impoundment.

Q3} What Coverage Should I Consider for a New Car?

- For a new car, consider comprehensive and collision coverage to protect your investment. Additionally, uninsured/underinsured motorist coverage is crucial in case of accidents involving other drivers with insufficient insurance.

Q4} Can I Transfer My Car Insurance to a New Vehicle?

- Yes, you can typically transfer your car insurance to a new vehicle. Contact your insurance provider to update your policy with the new vehicle's details.

Q5} Does Car Insurance Cover Rental Cars?

- Some car insurance policies extend coverage to rental cars. Check with your insurer to understand if your policy includes rental car coverage and any limitations.

Q6} Can I Lower My Premiums?

- Yes, you can potentially lower your premiums by maintaining a clean driving record, bundling policies, qualifying for discounts, and choosing a higher deductible.

Tags

#CarInsurance, #AutoInsurance, #CarInsuranceGuide, #CarInsuranceTips, #CarInsuranceCoverage, #CarInsurancePremiums, #CarInsuranceClaims, #NoFaultInsurance, #ChoosingDeductible, #CarInsuranceFAQs, #ComprehensiveCoverage, #LiabilityInsurance, #CarInsuranceBenefits, #CarInsuranceQuotes, #CarInsurancePolicy